Salary Pay Slip

Tlush Maskoret

תלוש משכורת

Last updated: 02.07.2023

This guide was adapted and translated by Shivat Zion. To see the original by T.M.L., click here.

The following guide is intended to provide an overview of various terms used in the Israeli workplace in connection with your employment. When in doubt about something related to your job, one should always seek out legal or professional advice.

The following guide is intended to provide an overview of various terms used in the Israeli workplace in connection with your employment. When in doubt about something related to your job, one should always seek out legal or professional advice.

Tlush Maskoret

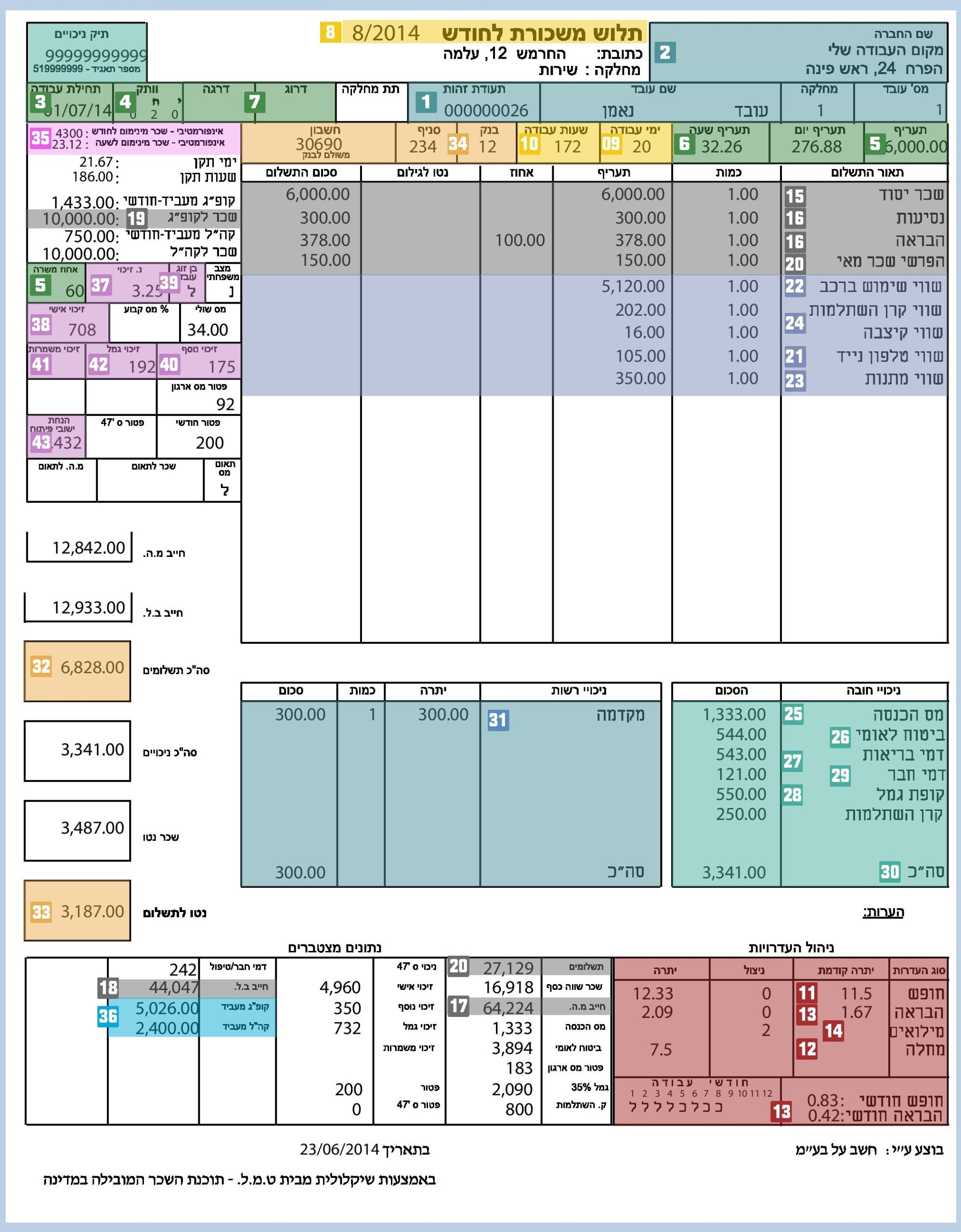

Every employed worker is required to receive a Tlush Maskoret – תלוש משכורת – Salary Pay Slip, at the end of every month from their employer along with their paid salary. Understanding how a Tlush is constructed is an excellent way to begin to understand your rights as a salaried employee. The following guide covers the main elements of the Tlush.

In order to better understand the guide you should open the link below and or print it out so you can follow along with the numbered items. Please note that this Tlush is just a sample and every company might have a different format. The key point is that every Tlush needs to provide the same relevant information as presented in our guide. As always, when in doubt about something you should consult with an accountant or lawyer.

Employer/Employee identification

- Last name and first name of the employee, including their Teudat Zehut number

- Employer’s name, their identification number/corporation number/tax deduction file number, and workplace address.

Terms of employment

- Start date of work

- Vetek Mitztaber – וותק מצטבר – accumulated seniority in the position (in days/months/years)

- For a salaried worker – who receives a monthly global salary, this is the gross base pay rate. One field #5 will reflect the salary amount, and the second field #5 reflects the percentage of a full-time position the job represents.

- For an hourly/daily/commission-based salaried worker – the number refers to the per-hour salary.

- This section is only relevant for an employee whose salary is based on a collective wage agreement. If they are, a letter or number will appear here depending on class, rank, level, or grade.

Pay-period for which payment is due

- The calendar month for which payment was made

- The number of actual potential working days in the above month

- The number of actual work hours for which the employee is being paid for

Absences and Additional Benefit Payments

Numbers 11-14 are presented in a chart where the columns, from right to left, represent – type of absence or benefit/previously accumulated days/how many days used this month/how many days are left

- Yemei Chufsha – ימי חופשה – Vacation days

- Yemei Machala – ימי מחלה – Sick days

- Dmei Havra’ah דמי הבראה an additional benefit payment- usually given once a year

- Milu’im – מילואים – days served in military reserve duty

Salary

Numbers 15-16 (and numbers 20-24 below) appear in the main chart on the Tlush. The columns correlate to description/quantity/tariff/percentage/total

- Sachar Yesod – שכר יסוד – Base salary

- Additional payments above the basic salary, including overtime, travel reimbursement, vacation payment, etc.

– Shaot Nosafot – שעות נוספות – Overtime

– Nesi’ot – נסיעות – Travel reimbursement

– Havra’a – הבראה - The sum of salary plus all other payments that are taxable by Mas Hachnasa – מס הכנסה Income Tax Authority, and their accumulated sum during the tax year so far.

- The sum of salary and all other payments that are used to calculate how much Bituach Leumi – ביטוח לאומי – National Insurance, will be deducted, and their accumulated sum during the tax year so far.

- Salary amount used to determine pension rights or other social welfare benefits, according to their type

- In an instance where the employee needs to supplement a salary from a previous month, it will appear here (In this example, the Tlush is for August 2014, but the sum in #20 includes an addition for salary from the month of May 2014). This is Hefresh Sachar – הפרש שכר – salary differential.

Additional Benefits that are Considered Income

- Cell phone – the monthly value of a cell phone that is assigned to the employee (if relevant)

- Vehicle allocation – the monthly tax value of a vehicle used by an employee (if relevant)

- Gift allocation – the gift value that an employee received (around holidays, for example)

- Kitzva – קצבה – allocation and/or Keren Hishtalmut – קרן השתלמות – professional development fund allocation (if relevant) – the amount of the sum put aside by the employee that is higher than the amount required by law and is therefore considered a Hatava – הטבה – benefit, and is taxable

Nikuyim - ניכויים - Compulsory Deductions

- Mas Hachnasa deduction

- Bituach Leumi deduction

- Bituach Bri’ut ביטוח בריאות Health insurance deduction

- The employee’s payment share to their Kupat Gemel – קופת גמל – pension fund savings

- An example of another deduction, by type

- The total of all deductions in this section

- An example of another optional deduction, by type

Payment details

- The Bruto – ברוטו – total (gross) salary

- The Neto – נטו – Net salary – actual take-home salary (Bruto minus the deductions)

- Bank information for direct deposit of salary (if relevant)

- Sometimes a Tlush might indicate here the monthly minimum wage and hourly minimum wage according to the law

- Employer’s share of payment for employees T’naim Sotzciali’im – תנאים סוציאליים – social benefits, that are deposited, not directly given to the employee, and not deducted from their salary, such as deposits to Keren Hishtalmut or Kupat Gemel.

- Nekudot Zikkuy – (.נקודות זיכוי (נ.ז – tax reduction points/credits. Nekudot Zikkuy are points that reflect a sum or amount that lowers the employee’s tax payments in a certain year based on their different eligibility. For example, points are given for being an Israeli citizen, for being a woman, by the number of children, for completing IDF service, for receiving an academic degree, etc.

- The monetary value of the Nekudot Zikkuy

- A Zikkuy/credit given in case the spouse of the employee is no longer working (this is an amount given when the spouse of the employee has already retired)

- Additional miscellaneous tax credits granted (if relevant)

- Additional tax credits granted to shift workers for overnight shifts

- Tax credit given to employees for their share of payments made towards their pensions

- 43. Additional tax credits granted to residents of development towns, rural areas and borderline communities according to the government’s official list